What Guideline F Actually Means in Plain English

Guideline F is the part of the security clearance system that evaluates financial considerations.

In plain English, it asks:

👉 Does this person’s financial situation create concern about judgment, reliability, responsibility, vulnerability, or willingness to meet obligations?

That does not mean the government expects every clearance applicant to be wealthy.

It does not mean debt automatically disqualifies you.

It does not mean bankruptcy automatically destroys your clearance.

And it does not mean one collection account or late payment always results in denial.

Guideline F is not about whether you are rich, poor, debt-free, or financially perfect.

It is about whether your financial record suggests risk.

That risk can come from several directions.

The government may worry that unresolved financial pressure could make someone vulnerable to:

- bribery

- coercion

- exploitation

- illegal financial shortcuts

- or desperate decision-making

The government may also worry that a long pattern of ignored obligations reflects:

- poor judgment

- unreliability

- lack of self-control

- unwillingness to follow rules

- or disregard for legal responsibilities

This is why financial problems are taken so seriously in clearance cases.

Money issues are not viewed only as personal problems.

They are viewed as potential security-risk indicators.

At National Security Law Firm, our security clearance lawyers include former adjudicators, former government attorneys, military lawyers, and national security insiders who understand how Guideline F is actually applied in real clearance decisions.

That insider perspective matters because applicants often misunderstand the issue.

They think the question is:

👉 “How much debt do I have?”

But adjudicators are usually asking a more important question:

👉 “What does this financial history say about this person’s judgment, reliability, and vulnerability going forward?”

That distinction matters enormously.

Two people can have similar debt amounts and very different outcomes.

One applicant may have debt caused by divorce, illness, job loss, military relocation, business failure, or identity theft—and may have taken responsible steps to resolve it.

Another applicant may have ignored bills for years, failed to file taxes, continued reckless spending, or hidden financial problems from the government.

Those are not the same clearance record.

In a Guideline F case, the issue is not just the balance owed.

The issue is:

👉 why the problem happened, what you did about it, and whether the record now supports trust.

Quick Answer: Can Debt Affect Your Security Clearance?

Yes.

Debt can absolutely affect your security clearance.

Financial concerns can result in:

- clearance delay

- additional investigation

- a Letter of Interrogatory

- a Statement of Reasons

- suspension

- denial

- or revocation

Common Guideline F issues include:

- credit card debt

- collections

- late payments

- unpaid taxes

- unfiled tax returns

- bankruptcy

- foreclosure

- repossession

- judgments

- student loan defaults

- gambling debt

- business debt

- unexplained affluence

- and financial problems that were not disclosed honestly

But this is the critical point:

👉 Debt alone does not automatically mean clearance denial.

Many people with debt hold security clearances.

Many people who filed bankruptcy hold security clearances.

Many people with tax debt, collections, or late payments can still obtain or keep clearances.

The question is usually not:

👉 “Do you have debt?”

The better question is:

👉 “Is the debt unresolved, ignored, unexplained, dishonest, or part of a broader pattern of financial irresponsibility?”

That is where cases become dangerous.

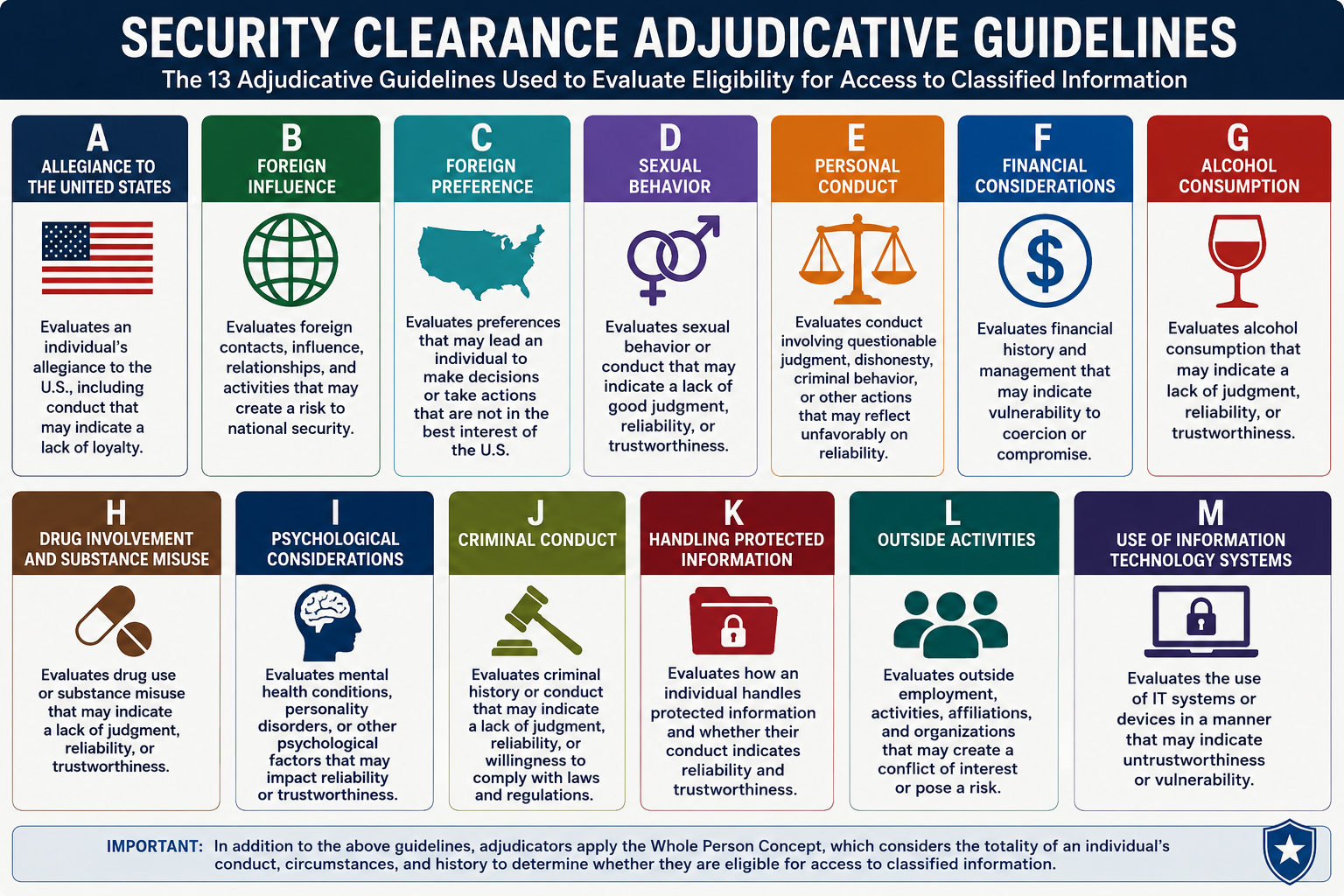

To understand how Guideline F fits into the broader clearance decision framework, review the

👉 Security Clearance Adjudicative Guidelines

Why Guideline F Is One of the Most Common Clearance Problems

Guideline F is one of the most common areas of concern in security clearance cases because financial information is easy to verify.

Credit reports create records.

Tax problems create records.

Collections create records.

Bankruptcies create records.

Judgments, liens, foreclosures, repossessions, and delinquent accounts often leave a paper trail.

That means financial problems are often discovered even when applicants do not expect them to be.

The government does not need to guess.

It can compare:

- SF-86 disclosures

- credit reports

- tax records

- court records

- bankruptcy filings

- debt documentation

- payment histories

- and interview explanations

This is why financial cases can escalate quickly.

An applicant may think:

👉 “It is just old debt.”

But the government may see:

👉 unpaid obligations, lack of resolution, and possible financial pressure.

An applicant may think:

👉 “I filed bankruptcy, so the problem is over.”

But the government may ask:

👉 “Why did the bankruptcy happen, and has the applicant shown stable financial behavior since?”

An applicant may think:

👉 “I am on a payment plan with the IRS.”

But the government may ask:

👉 “Are tax returns filed, is the agreement current, and did the applicant wait too long to address the issue?”

Guideline F cases are common because finances are measurable.

But they are also highly fact-specific.

The numbers matter.

The cause matters.

The timeline matters.

The response matters.

The documentation matters.

And honesty matters enormously.

Why Guideline F Cases Feel So Stressful

Guideline F cases can feel humiliating.

Money problems are personal.

Applicants often feel embarrassed about:

- credit card balances

- collections

- bankruptcy

- tax debt

- late payments

- foreclosure

- repossession

- gambling losses

- or needing help from family

Many applicants also feel frustrated because the financial problem may have been caused by circumstances outside their control.

They may think:

- “I got divorced.”

- “I lost my job.”

- “I had medical bills.”

- “My business failed.”

- “I was supporting family.”

- “I was deployed.”

- “I was trying to keep my household together.”

- “I filed bankruptcy responsibly.”

Those facts may matter.

But they must be presented correctly.

Because adjudicators are not only evaluating whether the financial hardship was understandable.

They are evaluating whether the applicant responded responsibly.

That is the key distinction.

The government may be sympathetic to hardship.

But sympathy alone does not resolve security concern.

A strong Guideline F case must usually show:

👉 the financial problem was caused by understandable circumstances, and the applicant took credible steps to address it.

That is where many applicants make mistakes.

They explain the hardship but do not prove the recovery.

They describe the debt but do not document the plan.

They blame the creditor but do not show a formal dispute.

They say they are “working on it” but provide no evidence.

They say the issue is old but show no current financial stability.

Guideline F cases are not won through embarrassment or explanation alone.

They are won through:

👉 documentation, responsibility, consistency, and proof of financial control.

Why the Insider Perspective Matters in Financial Clearance Cases

Most online advice about financial clearance problems says:

👉 “Pay your debts.”

That is true.

But it is incomplete.

The harder question is:

👉 What does the adjudicator need to see before they feel comfortable approving the clearance?

At National Security Law Firm, we approach Guideline F cases from the perspective of the decision-maker.

Our attorneys understand how adjudicators evaluate:

- the cause of debt

- the amount of debt

- the age of debt

- the frequency of delinquency

- whether the problem was voluntary or beyond the applicant’s control

- whether the applicant ignored the issue

- whether there is a realistic repayment plan

- whether payments are current

- whether taxes are filed

- whether bankruptcy resolved the problem

- whether financial behavior has changed

- whether disclosures were honest

- and whether approval can be defended despite the financial record

That last question matters.

In security clearance cases, the issue is not merely whether the applicant has an explanation.

The issue is whether the record makes approval defensible.

For example:

An applicant with $50,000 in debt but strong documentation, a repayment plan, stable income, and a clear hardship explanation may be in a much better position than an applicant with $8,000 in ignored collections and no plan.

Why?

Because the first file may show responsibility.

The second may show avoidance.

That is the real difference.

Guideline F cases are often won or lost on whether the applicant can show:

👉 financial responsibility despite financial difficulty.

What This Guide Will Help You Understand

If you are dealing with a Guideline F issue—or worried that one may arise—this guide will explain:

- what financial considerations actually mean

- why debt can affect a security clearance

- when debt becomes a clearance problem

- how bankruptcy is evaluated

- why unpaid taxes and unfiled returns are especially serious

- how collections and late payments are reviewed

- why gambling debt creates additional concern

- how financial problems can overlap with lack of candor

- what adjudicators actually look for

- where financial clearance cases fail

- and how strong cases are built around documentation, responsibility, and financial control

Most importantly, this guide will help you understand how the government views financial problems from a security-risk perspective.

Because until you understand that:

👉 you may be trying to explain debt while the government is evaluating reliability, vulnerability, and future judgment.

That mismatch is where many Guideline F cases begin to fail.

When Guideline F Actually Comes Up in Real Cases

Guideline F issues usually arise when the government believes:

👉 the applicant’s financial history reflects unresolved risk, instability, irresponsibility, or vulnerability to pressure.

Sometimes the issue involves extremely large debt.

More often, the issue begins with patterns.

Examples include:

- repeated late payments

- unresolved collections

- unfiled tax returns

- ignored debt

- foreclosure

- repossession

- gambling losses

- excessive credit-card usage

- bankruptcy

- or financial problems that continue without a clear resolution plan

That is why many applicants are surprised when Guideline F appears.

They often think:

👉 “Lots of people have debt.”

That is true.

But adjudicators are not evaluating debt in the abstract.

They are evaluating:

👉 whether the financial situation suggests future reliability or future vulnerability problems.

Below are some of the most common ways Guideline F appears in real clearance cases.

Credit Card Debt

Credit card debt is one of the most common Guideline F issues.

Debt itself is not automatically disqualifying.

Many clearance holders carry balances.

The issue becomes dangerous when the debt appears:

- excessive relative to income

- unresolved

- repeatedly delinquent

- ignored

- or part of a larger pattern of financial instability

Adjudicators often evaluate:

- total balances

- minimum payments

- missed-payment history

- debt-to-income ratio

- use of credit for necessities versus discretionary spending

- and whether the applicant has a realistic plan to regain control

Applicants often make the mistake of focusing only on:

👉 “how much debt.”

But adjudicators usually care more about:

👉 how the applicant is managing the debt now.

For deeper analysis, review:

👉 Can You Lose Your Security Clearance for Debt?

👉 Debt and Security Clearances

Collections and Late Payments

Collections and chronic late payments are another major Guideline F trigger.

Applicants often underestimate how damaging unresolved collections can look.

Especially where:

- accounts were ignored for long periods

- no payment plan exists

- multiple creditors are involved

- or the applicant minimized the issue during investigation

The issue is often not:

👉 the existence of the collection itself.

The issue is:

👉 whether the applicant appears unwilling or unable to manage obligations responsibly.

For deeper analysis, review:

👉 Can You Lose Your Security Clearance for Collections or Late Payments?

Unpaid Taxes and Unfiled Returns

Tax problems are among the most serious financial issues in security clearance law.

Why?

Because taxes involve:

👉 legal obligations owed directly to the government.

Adjudicators often view unpaid taxes differently from ordinary debt because failure to:

- file returns

- pay taxes

- or resolve IRS obligations

can suggest:

- disregard for legal responsibilities

- poor judgment

- unwillingness to comply with rules

- or avoidance behavior

Applicants frequently think:

👉 “I was overwhelmed.”

Or:

👉 “I planned to deal with it later.”

But adjudicators often focus heavily on:

- whether returns are now filed

- whether payment plans exist

- whether payments are current

- and whether the applicant ignored the issue for years

Tax issues become especially dangerous when:

- multiple years remain unfiled

- the applicant concealed the issue

- or no active resolution effort exists

For deeper analysis, review:

👉 Can You Lose Your Security Clearance for Unpaid Taxes?

👉 What You Should Know About Filing Your Taxes and Security Clearance

Bankruptcy

Bankruptcy is one of the most misunderstood areas of Guideline F.

Many applicants believe:

👉 “Bankruptcy automatically destroys clearance eligibility.”

That is not true.

In many situations, bankruptcy may actually help mitigation because it demonstrates:

👉 active effort to resolve overwhelming debt responsibly.

Adjudicators usually focus less on:

👉 the existence of the bankruptcy itself

and more on:

- why it happened

- whether the applicant acted responsibly afterward

- whether financial behavior improved

- and whether the bankruptcy stabilized the financial situation

A bankruptcy caused by:

- divorce

- medical hardship

- job loss

- business collapse

- or economic downturn

may look very different than bankruptcy caused by:

👉 repeated reckless spending with no behavioral change afterward.

For deeper analysis, review:

👉 Can You Lose Your Security Clearance for Bankruptcy?

👉 Bankruptcy and Security Clearances: How Adjudicators Actually Evaluate Financial Risk

Foreclosure, Repossession, and Judgments

Foreclosures, repossessions, and civil judgments are major financial indicators because they create:

👉 documented evidence of unresolved financial obligations.

Adjudicators often evaluate:

- why the event occurred

- whether the applicant attempted resolution

- whether the issue was voluntary or unavoidable

- and whether similar problems continue today

A foreclosure caused by sudden unemployment may be viewed differently than:

👉 repeated mortgage delinquency combined with ongoing overspending.

Again:

👉 context matters enormously.

Student Loan Problems

Student loans are extremely common.

Student loan debt alone is usually not disqualifying.

The issue becomes more serious when loans are:

- delinquent

- in default

- ignored

- or repeatedly unresolved

Adjudicators often evaluate:

- whether the applicant is in repayment

- whether deferment or rehabilitation exists

- whether payments are current

- and whether the issue is improving or worsening

Many student-loan cases are highly mitigable when the applicant demonstrates:

👉 active and responsible repayment efforts.

Medical Debt

Medical debt is often viewed differently from consumer debt because it may arise from:

👉 circumstances beyond the applicant’s control.

This is one of the strongest mitigation themes in Guideline F.

Applicants often improve their position significantly when they can document:

- serious illness

- emergency medical expenses

- insurance failures

- or family medical hardship

while also demonstrating:

👉 responsible efforts to address the debt afterward.

Divorce-Related Debt

Divorce is another extremely common source of financial problems in clearance cases.

Examples include:

- legal fees

- support obligations

- property division problems

- shared debt defaults

- or sudden household-income disruption

Adjudicators often evaluate:

- whether the applicant responded responsibly

- whether obligations are now current

- and whether the financial instability appears temporary or ongoing

Business Failure or Job Loss

Many financially responsible people experience severe setbacks after:

- layoffs

- failed businesses

- economic downturns

- or contract loss

These situations are often highly mitigable when applicants demonstrate:

- good-faith recovery efforts

- active employment pursuit

- restructuring

- payment plans

- or bankruptcy used responsibly

The key is usually not the hardship itself.

The key is:

👉 how the applicant handled the hardship afterward.

Gambling Debt

Gambling-related debt often creates additional concern because it may suggest:

- impulse-control problems

- addiction

- desperation

- concealment

- or escalating financial instability

Adjudicators often evaluate:

- frequency of gambling

- debt amounts

- borrowing behavior

- concealment of losses

- and whether treatment or recovery efforts exist

For deeper analysis, review:

👉 Can You Lose Your Security Clearance for Gambling Debt?

Unexplained Affluence

Guideline F is not only about debt.

It also covers:

👉 unexplained wealth.

Adjudicators may become concerned where:

- assets appear inconsistent with income

- cash flow is unclear

- foreign funds appear unexplained

- or expensive lifestyles lack credible financial support

The issue is not simply wealth.

The issue is:

👉 whether the source of wealth can be trusted and explained.

Financial Problems Combined With Nondisclosure

This is where Guideline F often becomes much more dangerous.

Applicants sometimes:

- omit debt from the SF-86

- hide tax issues

- minimize collections

- conceal bankruptcy

- or fail to disclose financial judgments

Once financial issues become:

👉 honesty problems

the case may expand into:

👉 Guideline E — Personal Conduct

This is one of the most important realities of Guideline F:

👉 the debt itself is often less dangerous than dishonesty about the debt.

The Guideline F Statute (Full Text)

The full statutory language for Guideline F can be reviewed here:

👉 Guideline F — Financial Considerations (Full Text)

The regulation explains:

- what financial conduct raises concern

- how adjudicators evaluate financial responsibility

- and what mitigating conditions may apply

But reading the statute alone is not enough.

Because Guideline F cases are rarely decided based solely on:

👉 the existence of debt.

They are decided based on:

- cause

- timing

- responsibility

- repayment efforts

- documentation

- and whether the adjudicator believes the applicant remains financially trustworthy going forward

That is why two applicants with similar debt levels may receive completely different outcomes.

👉 The difference is often not the amount of debt.

👉 It is how the applicant handled the financial problem afterward.

What the Government Is Actually Worried About

To truly understand Guideline F, you have to understand the government’s core concern.

The government is not trying to punish people for having financial hardship.

It is evaluating:

👉 whether financial problems create security risk.

That concern generally falls into several categories.

1. Vulnerability to Coercion or Bribery

This is one of the oldest concerns in clearance law.

The government worries that severe unresolved financial pressure may make an applicant vulnerable to:

- bribery

- coercion

- espionage recruitment

- or desperate financial decision-making

This is why unresolved debt is treated seriously.

2. Judgment and Reliability

Guideline F is heavily focused on judgment.

Adjudicators evaluate whether financial conduct reflects:

- irresponsibility

- recklessness

- avoidance

- lack of planning

- or unwillingness to meet obligations

Again:

👉 the issue is often not the debt itself.

It is:

👉 what the debt suggests about future reliability.

3. Willingness to Meet Legal Obligations

This is especially important in tax cases.

Adjudicators evaluate whether applicants:

- file returns

- pay obligations

- follow court orders

- and address financial responsibilities proactively

Failure to do so may suggest:

👉 disregard for rules and obligations.

4. Concealment and Credibility Problems

Once financial issues are hidden, minimized, or omitted:

👉 the case often becomes more serious.

This is where Guideline F overlaps heavily with:

👉 Guideline E — Personal Conduct.

5. Future Financial Stability

Ultimately, Guideline F is predictive.

The government is asking:

👉 “Does this financial record suggest future instability or future security risk?”

That is the real issue driving most Guideline F decisions.

How Adjudicators Actually Evaluate Guideline F Cases

This is where insider perspective matters most.

Adjudicators do not evaluate Guideline F mechanically.

They do not simply ask:

👉 “How much debt does the applicant have?”

They ask:

👉 “What does this financial history tell me about this applicant’s judgment, reliability, honesty, vulnerability, and future stability?”

That distinction is critical.

Because many Guideline F cases are not really about the debt itself.

They are about:

👉 whether the applicant appears financially responsible despite the debt.

Adjudicators often evaluate several core questions.

What Caused the Financial Problem?

This is one of the most important issues in Guideline F.

Adjudicators often distinguish between debt caused by:

- divorce

- illness

- layoffs

- military relocation

- identity theft

- economic downturns

- business failure

- or emergencies

versus debt caused by:

- reckless spending

- gambling

- substance abuse

- irresponsibility

- fraud

- or chronic financial neglect

Applicants frequently misunderstand this distinction.

They focus only on:

👉 the amount of debt.

But adjudicators usually care just as much about:

👉 the reason the debt exists.

Did the Applicant Ignore the Problem?

This is one of the biggest issues in Guideline F.

Debt itself is often manageable.

Ignored debt is much more dangerous.

Adjudicators heavily evaluate whether the applicant:

- stopped communicating with creditors

- ignored collection notices

- failed to file taxes

- failed to create payment plans

- or avoided dealing with financial obligations for long periods

This is one reason applicants who take proactive steps early often perform much better than applicants who wait until:

👉 the clearance investigation forces action.

Is There a Realistic Resolution Plan?

Strong financial cases usually involve:

👉 evidence of active resolution.

Adjudicators often look for:

- repayment plans

- settlement agreements

- current payments

- bankruptcy filings

- tax agreements

- counseling

- consolidation efforts

- loan rehabilitation

- or documented budgeting improvements

The government does not necessarily expect instant financial perfection.

But it often expects:

👉 responsible forward movement.

Is the Financial Behavior Still Ongoing?

Timing matters enormously.

Adjudicators evaluate:

- whether delinquencies are current

- whether new debt continues accumulating

- whether gambling continues

- whether taxes remain unfiled

- and whether the applicant appears financially stable now

This is one reason older financial problems are often easier to mitigate than:

👉 active unresolved instability.

Was the Financial Situation Disclosed Honestly?

This is where many Guideline F cases become much more dangerous.

Applicants sometimes:

- omit debt

- hide tax problems

- fail to disclose collections

- minimize judgments

- or conceal bankruptcies

Once that happens:

👉 the case often expands into a Guideline E credibility problem.

This is one of the most important realities of financial clearance law:

👉 the debt itself is often less dangerous than dishonesty about the debt.

Can Approval Be Defended?

This is one of the most important insider concepts in clearance law.

Adjudicators constantly ask themselves:

👉 “Could I defend approving this applicant later if this file were reviewed?”

That question drives many Guideline F outcomes.

If the record feels:

- documented

- improving

- financially controlled

- and responsibly managed

approval becomes much more likely.

If the file feels:

- ignored

- evasive

- unstable

- undocumented

- or financially reckless

approval becomes much harder.

Debt and Security Clearances

Debt is one of the most searched security clearance topics because applicants often assume:

👉 “Debt automatically disqualifies me.”

That is not true.

Many people with debt successfully obtain and maintain security clearances.

The issue is usually not:

👉 whether debt exists.

The issue is:

👉 whether the debt creates unresolved concern about judgment, reliability, or vulnerability.

For example:

A person carrying large balances but making regular payments and maintaining stable finances may look very different than:

👉 someone ignoring smaller debts for years with no plan.

This is why:

👉 debt management matters more than debt existence alone.

For deeper analysis, review:

👉 Can You Lose Your Security Clearance for Debt?

👉 Debt and Security Clearances

Bankruptcy and Security Clearances

Bankruptcy is one of the most misunderstood areas of Guideline F.

Applicants often panic because they assume:

👉 “Bankruptcy means automatic denial.”

But bankruptcy can actually improve some cases because it may demonstrate:

👉 responsible effort to resolve overwhelming debt.

Adjudicators usually focus on:

- why the bankruptcy happened

- whether it solved the financial instability

- whether financial behavior improved afterward

- and whether the applicant now appears financially stable

Bankruptcy caused by:

- illness

- divorce

- layoffs

- business collapse

- or unavoidable hardship

may look very different than bankruptcy tied to:

👉 chronic reckless behavior with no change afterward.

For deeper analysis, review:

👉 Can You Lose Your Security Clearance for Bankruptcy?

👉 Bankruptcy and Security Clearances: How Adjudicators Actually Evaluate Financial Risk

Taxes and Security Clearances

Tax problems are among the most serious financial concerns in clearance law.

This is because taxes involve:

👉 obligations owed directly to the government.

Adjudicators often view unfiled returns and unpaid taxes differently than ordinary consumer debt.

Applicants frequently think:

👉 “I was overwhelmed.”

Or:

👉 “I planned to deal with it later.”

But adjudicators often focus heavily on:

- whether returns are filed now

- whether payment agreements exist

- whether payments are current

- and whether the applicant ignored the issue for years

This is one reason tax cases become dangerous quickly.

Especially where:

- multiple years remain unfiled

- the applicant minimized the issue

- or no active resolution effort exists

For deeper analysis, review:

👉 Can You Lose Your Security Clearance for Unpaid Taxes?

👉 What You Should Know About Filing Your Taxes and Security Clearance

Collections and Late Payments

Collections and chronic late payments create concern because they suggest:

👉 unresolved financial instability.

Applicants often underestimate how damaging ignored collections can look.

Especially where:

- multiple accounts exist

- payments stopped entirely

- no payment plan exists

- or the issue remained unresolved for years

Again:

👉 the issue is often not the collection itself.

The issue is:

👉 whether the applicant appears unwilling or unable to manage obligations responsibly.

For deeper analysis, review:

👉 Can You Lose Your Security Clearance for Collections or Late Payments?

Gambling Debt

Gambling debt often creates heightened concern because it may suggest:

- compulsive behavior

- desperation

- concealment

- poor impulse control

- or escalating financial instability

Adjudicators often evaluate:

- frequency of gambling

- debt accumulation

- borrowing behavior

- hidden losses

- and whether treatment or recovery exists

This is one reason gambling-related financial cases often become more serious than ordinary debt cases.

For deeper analysis, review:

👉 Can You Lose Your Security Clearance for Gambling Debt?

Cleaning Up Finances Before Applying for Clearance

Many applicants ask:

👉 “Should I wait to apply until my finances are perfect?”

Not necessarily.

But proactive financial cleanup can dramatically improve a clearance case.

Strong preparation often includes:

- reviewing credit reports

- filing missing tax returns

- documenting disputes

- creating payment plans

- resolving active collections where possible

- reducing delinquency patterns

- and avoiding new financial instability

Applicants who proactively stabilize finances before submission often create:

👉 much cleaner adjudicative records.

For deeper analysis, review:

👉 How to Clean Up Your Finances Before Applying for Clearance

The “Debt Is Not the Problem, Ignoring Debt Is the Problem” Framework

This is one of the most important Guideline F concepts.

Many applicants believe:

👉 “I need zero debt to keep my clearance.”

That is not true.

Adjudicators often distinguish sharply between:

👉 people experiencing financial hardship

and

👉 people refusing to deal with financial hardship responsibly.

A person with large debt but:

- payment plans

- tax compliance

- active budgeting

- counseling

- and documented financial recovery

may present far less concern than:

👉 a person with smaller debt who ignored obligations entirely.

This is why:

👉 responsible response often matters more than the original financial problem itself.

The “Paper Risk” Problem in Guideline F Cases

This is one of the most important concepts in all clearance law.

Even manageable financial problems can become dangerous when:

👉 the record itself feels unstable or unsupported.

This is what we call:

👉 paper risk.

Examples include:

- vague hardship explanations

- undocumented payment plans

- inconsistent debt disclosures

- missing tax documentation

- emotional financial narratives

- reactive cleanup only after investigation

- or unclear timelines

Once the file begins to feel:

- financially unstable

- evasive

- undocumented

- or difficult to defend

👉 adjudicators become uncomfortable approving it.

That discomfort matters enormously.

Because adjudicators constantly ask themselves:

👉 “Can I defend approving this applicant later?”

If the answer becomes uncertain:

👉 the case becomes much harder to win.

What Strong Guideline F Mitigation Actually Looks Like

Strong Guideline F mitigation is not built around emotional explanation alone.

It is built around:

👉 documented financial responsibility and credible future stability.

That distinction is critical.

Because adjudicators are not simply evaluating whether the applicant feels bad about the debt.

They are evaluating:

👉 whether the applicant now appears financially reliable and unlikely to become a future security risk.

Strong mitigation often includes several recurring themes.

Good-Faith Effort to Resolve Debt

This is one of the strongest mitigation factors in Guideline F.

Applicants who actively address debt usually perform far better than applicants who:

👉 ignore the problem until the clearance process forces action.

Strong examples include:

- payment plans

- settlement agreements

- debt consolidation

- bankruptcy used responsibly

- loan rehabilitation

- IRS installment agreements

- or documented creditor negotiations

The government does not necessarily require every debt to be fully paid immediately.

But it often expects:

👉 credible effort and forward progress.

Documented Financial Hardship

One of the strongest mitigation themes involves circumstances beyond the applicant’s control.

Examples include:

- divorce

- illness

- layoffs

- military relocation

- economic downturns

- family emergencies

- identity theft

- or failed business ventures

But hardship alone is not enough.

Adjudicators also evaluate:

👉 what the applicant did after the hardship occurred.

Strong cases usually combine:

- credible hardship documentation

with - evidence of responsible recovery efforts

Current Financial Stability

Guideline F is heavily future-focused.

Adjudicators want to see:

👉 present financial control.

Strong cases often include evidence such as:

- stable employment

- current payments

- reduced balances

- improved credit history

- filed tax returns

- active budgeting

- savings growth

- or consistent repayment behavior

This is one reason older financial problems are often easier to mitigate than:

👉 active ongoing instability.

Tax Compliance

Tax compliance is one of the most important areas in Guideline F mitigation.

Applicants with tax problems usually improve their position dramatically when they:

- file all missing returns

- enter payment agreements

- remain current on payments

- and maintain compliance afterward

This is because tax compliance demonstrates:

👉 willingness to meet legal obligations.

Financial Counseling or Rehabilitation

Financial counseling can help some Guideline F cases significantly.

This may include:

- credit counseling

- debt-management programs

- financial education

- budgeting assistance

- or gambling treatment where appropriate

Counseling can demonstrate:

👉 insight, responsibility, and proactive correction.

Strong Whole-Person Evidence

Guideline F cases are heavily influenced by:

👉 the Whole Person Concept.

Adjudicators may consider:

- military service

- federal service

- professional evaluations

- character references

- security history

- financial recovery progress

- and evidence of otherwise responsible conduct

This is especially important where the financial hardship appears inconsistent with the applicant’s broader life history.

What Weak Guideline F Mitigation Looks Like

Weak mitigation usually shares one common theme:

👉 the applicant appears financially reactive instead of financially responsible.

Applicants often damage their cases by saying things like:

- “I’ll deal with it eventually.”

- “Everyone has debt.”

- “I just ignored the letters.”

- “I didn’t think taxes mattered that much.”

- “I planned to handle it later.”

- “I only started paying after the SOR.”

Those explanations often fail because adjudicators may interpret them as:

👉 ongoing irresponsibility or avoidance behavior.

The “I Was Overwhelmed” Problem

Applicants often explain:

👉 “I was overwhelmed.”

That may be true.

But adjudicators frequently ask:

👉 “What did the applicant do despite being overwhelmed?”

Strong cases usually involve some evidence of:

- effort

- communication

- planning

- or responsible action

Weak cases often show:

👉 complete avoidance.

That distinction matters enormously.

Reactive Cleanup Is One of the Biggest Problems in Guideline F Cases

Applicants often wait until:

- the background investigation

- the LOI

- the SOR

- or the hearing

before taking action.

This creates one of the biggest dangers in Guideline F:

👉 reactive mitigation.

Adjudicators often distinguish sharply between:

👉 proactive financial responsibility

and

👉 last-minute cleanup after discovery.

Late cleanup can still help.

But the strategic value is often very different.

Undocumented Payment Plans Quietly Hurt Cases

Applicants often say:

👉 “I’m working on it.”

But adjudicators want documentation.

Strong cases often include:

- payment-plan agreements

- tax-plan confirmations

- settlement documentation

- payment receipts

- bankruptcy filings

- or counseling records

Without documentation:

👉 the financial recovery narrative becomes much weaker.

Advanced Strategy: How to Respond to a Guideline F Concern

Guideline F cases require strategic financial storytelling.

Because adjudicators are not just evaluating debt.

They are evaluating:

👉 reliability, control, vulnerability, and future judgment.

This is why the response strategy matters so much.

Strategy Shift #1: Stop Thinking the Debt Alone Decides the Case

Many applicants panic because they think:

👉 “The number itself destroys me.”

That is not usually true.

The stronger strategic question is:

👉 “What does the debt record suggest about my judgment and future reliability?”

That is what adjudicators actually evaluate.

Strategy Shift #2: Focus on Financial Recovery, Not Financial Excuses

Applicants often spend too much time explaining:

👉 why the debt happened.

That matters.

But adjudicators also need to see:

👉 what changed afterward.

Strong cases therefore focus heavily on:

- repayment efforts

- stabilization

- planning

- budgeting

- and current financial control

Strategy Shift #3: Document Everything

This is one of the most important strategic rules in Guideline F.

Financial mitigation without documentation is weak.

Strong cases usually include:

- payment history

- settlement records

- bankruptcy documents

- tax filings

- repayment plans

- counseling records

- and current financial snapshots

This helps transform:

👉 explanation

into:

👉 verifiable mitigation evidence.

Strategy Shift #4: Avoid Financial Minimization

Applicants frequently damage their cases by minimizing obvious financial instability.

Examples include:

- “It’s not that much debt.”

- “Everyone has collections.”

- “I only missed taxes for a few years.”

- “I’ll get to it eventually.”

Those explanations often create more concern—not less.

Because adjudicators may interpret them as:

👉 lack of insight into the seriousness of the issue.

Strategy Shift #5: Focus on Future Stability

Ultimately, Guideline F is predictive.

The adjudicator is asking:

👉 “Does this financial history create future security risk?”

That means strong mitigation focuses heavily on:

- present stability

- realistic repayment

- current compliance

- and why the problem is unlikely to recur

Illustrative Guideline F Case Scenarios

The examples below are hypothetical scenarios based on common fact patterns seen in security clearance cases. They are designed to show how adjudicators typically evaluate Guideline F concerns—not to predict outcomes in any specific case.

Scenario 1 — Divorce-Related Debt With Active Repayment (Often Mitigable)

An applicant accumulates significant credit-card debt during a divorce and temporary loss of household income.

The applicant:

- enters repayment plans

- remains current on payments

- documents the divorce hardship

- and demonstrates stable employment afterward

👉 Likely Outcome: Often mitigable

Why this works:

The debt appears tied to understandable hardship and responsible recovery efforts exist.

Scenario 2 — Ignored Tax Debt for Years (High Risk)

An applicant failed to file tax returns for multiple years and only began addressing the issue after receiving an SOR.

👉 Likely Outcome: Significant Guideline F concern

Why this creates concern:

Long-term tax noncompliance suggests disregard for legal obligations.

Scenario 3 — Bankruptcy After Medical Crisis (Often Mitigable)

An applicant files bankruptcy after severe medical debt and job disruption.

The applicant:

- completed bankruptcy responsibly

- stabilized finances afterward

- and accumulated no new delinquent debt

👉 Likely Outcome: Often manageable

Why this works:

The bankruptcy appears to have resolved—not worsened—the financial instability.

Scenario 4 — Gambling Debt With Ongoing Gambling (High Risk)

An applicant accumulates large gambling losses while continuing active gambling behavior.

👉 Likely Outcome: Severe concern

Why this creates concern:

The problem appears ongoing and tied to poor impulse control.

Scenario 5 — Collections Ignored Until Investigation (Moderate to High Risk)

An applicant has multiple collections but made no repayment efforts until investigators raised the issue.

👉 Likely Outcome: More difficult mitigation

Why this creates concern:

The record suggests reactive rather than responsible financial behavior.

Scenario 6 — Debt Dispute Supported by Documentation (Potentially Mitigable)

An applicant disputes several debts resulting from identity theft and provides:

- police reports

- dispute filings

- and creditor correspondence

👉 Likely Outcome: Potentially manageable

Why this helps:

The applicant documented legitimate dispute efforts and appears proactive.

Scenario 7 — Strong Financial Cleanup Before Applying (Strong Mitigation)

An applicant reviews credit reports before applying, resolves collections, files missing taxes, and documents repayment plans before submitting the SF-86.

👉 Likely Outcome: Stronger clearance position

Why this works:

The applicant proactively stabilized the financial record before adjudication.

Scenario 8 — Debt Plus Dishonesty About Debt (Severe Risk)

An applicant omits major delinquent debt from the SF-86.

👉 Likely Outcome: Guideline F plus Guideline E concern

Why this creates concern:

The concealment often becomes more dangerous than the debt itself.

What Actually Gets Guideline F Cases Approved

Successful Guideline F cases usually share several characteristics.

The applicant typically:

- explains the cause of the debt credibly

- documents hardship appropriately

- demonstrates active repayment or resolution

- files taxes and maintains compliance

- shows financial behavior improvement

- avoids new delinquency patterns

- and discloses the issue honestly

Most importantly:

👉 the adjudicator ultimately believes the applicant is financially responsible going forward.

That is the real issue in Guideline F.

Not perfection.

👉 future financial reliability.

What Causes Guideline F Denials

Guideline F denials usually stem from one core conclusion:

👉 the adjudicator believes the applicant’s financial situation still creates unresolved security risk.

That concern may involve:

- vulnerability to coercion

- chronic irresponsibility

- poor judgment

- ongoing instability

- disregard for legal obligations

- or dishonesty surrounding financial problems

This is one of the most important realities of Guideline F:

👉 the denial often happens because the adjudicator concludes the financial problems remain unresolved—not simply because debt exists.

Unresolved Debt Is One of the Biggest Problems

Debt itself is often manageable.

But debt that remains:

- ignored

- undocumented

- unresolved

- or continuously worsening

creates much greater concern.

Adjudicators often deny cases where applicants:

- have no payment plan

- stopped communicating with creditors

- ignored tax obligations

- or continued accumulating delinquent debt without corrective action

Again:

👉 the issue is often not the balance itself.

The issue is:

👉 whether the applicant appears financially out of control.

Tax Problems Frequently Drive Denials

Unfiled returns and unresolved tax debt are among the most dangerous financial issues in clearance law.

Especially where:

- multiple years remain unfiled

- the applicant ignored IRS notices

- payment plans do not exist

- or the applicant minimized the seriousness of the issue

This is because tax cases often suggest:

👉 unwillingness to comply with legal obligations.

That creates broader trustworthiness concerns beyond simple debt.

Gambling Debt Creates Heightened Risk

Gambling-related financial instability often creates additional concern because adjudicators may view it as:

- compulsive

- escalating

- concealed

- or difficult to control

Especially where:

- gambling continues

- losses remain hidden

- or the applicant borrowed money irresponsibly

This is one reason gambling debt cases often become much more difficult than ordinary consumer-debt cases.

Financial Problems Combined With Dishonesty

This is where many Guideline F cases become significantly more dangerous.

Applicants sometimes:

- omit debt from the SF-86

- conceal collections

- hide tax problems

- fail to disclose bankruptcies

- or provide inconsistent financial explanations

Once financial issues become:

👉 credibility problems

the case frequently expands into:

👉 Guideline E — Personal Conduct

And once dishonesty enters the file:

👉 mitigation becomes substantially harder.

Where Guideline F Cases Collapse

Most Guideline F cases do not fail simply because debt exists.

They fail during escalation.

This is one of the most important concepts in financial clearance law.

Stage 1 — Financial Trouble Begins

Examples:

- divorce

- illness

- layoffs

- tax problems

- gambling losses

- overspending

- or business failure

At this stage:

👉 the issue may still be highly manageable.

Stage 2 — Debt or Delinquency Expands

Collections, late payments, judgments, or tax problems begin accumulating.

The applicant often becomes:

- overwhelmed

- embarrassed

- avoidant

- or financially reactive

Stage 3 — The Applicant Stops Addressing the Problem

This is one of the most dangerous moments.

Examples include:

- ignoring creditors

- avoiding taxes

- failing to create payment plans

- or simply hoping the issue disappears

Now adjudicators begin seeing:

👉 unresolved financial irresponsibility.

Stage 4 — Investigation or Credit Review Reveals the Problem

The debt appears during:

- SF-86 review

- credit checks

- tax review

- background investigation

- or subject interviews

At this stage, adjudicators begin asking:

👉 “What has the applicant done to resolve this?”

Stage 5 — Explanations Become Weak or Unsupported

Applicants often damage their cases by saying:

- “I was going to deal with it.”

- “I didn’t think it mattered.”

- “Everyone has debt.”

- “I just got overwhelmed.”

without providing:

👉 documentation or active resolution evidence.

Stage 6 — Guideline E Overlap Appears

If the applicant:

- omitted debt

- concealed taxes

- minimized financial problems

- or gave inconsistent financial disclosures

the case may now expand into:

👉 a Guideline E credibility problem.

At this point:

👉 mitigation becomes significantly harder.

Stage 7 — SOR or Denial

The unresolved financial concern hardens into:

- an LOI

- a Statement of Reasons

- suspension

- denial

- or revocation

👉 Final outcome: denial or clearance loss.

How Guideline F Interacts With Other Guidelines

Guideline F frequently overlaps with several other security clearance guidelines.

This is one reason financial cases can become more complicated than applicants expect.

Guideline E — Personal Conduct

This is the most common overlap.

Examples include:

- omitting debt

- hiding tax problems

- concealing bankruptcy

- false financial disclosures

- or inconsistent explanations

In many cases:

👉 the dishonesty becomes more dangerous than the debt itself.

See:

👉 Guideline E — Personal Conduct

Guideline B — Foreign Influence

Financial support sent overseas or dependence on foreign financial assistance may overlap with:

👉 foreign influence concerns.

Examples include:

- financially supporting foreign family

- receiving foreign financial support

- or maintaining unresolved foreign financial obligations

See:

👉 Guideline B — Foreign Influence

Guideline G — Alcohol Consumption

Financial problems caused by alcohol-related behavior may create overlapping Guideline G concerns.

Examples include:

- DUIs causing financial collapse

- alcohol-related employment problems

- or repeated alcohol-related spending patterns

See:

👉 Guideline G — Alcohol Consumption

Guideline H — Drug Involvement

Drug-related financial instability may create overlapping concerns involving:

- addiction

- financial irresponsibility

- or concealment

See:

👉 Guideline H — Drug Involvement and Substance Misuse

Guideline J — Criminal Conduct

Fraud, theft, tax crimes, embezzlement, or other illegal financial activity may trigger:

👉 criminal conduct concerns.

See:

👉 Guideline J — Criminal Conduct

👉 Once multiple guidelines apply, the mitigation burden often becomes much heavier.

How Guideline F Appears Throughout the Clearance Process

Financial concerns can emerge at nearly every stage of the security clearance process.

Many applicants mistakenly assume:

👉 “If I explain the debt once, the issue goes away.”

That is not how the system works.

Financial concerns often follow applicants throughout:

- the SF-86 process

- credit-report review

- the background investigation

- subject interviews

- LOIs

- SORs

- hearings

- and future reinvestigations or continuous vetting

This is why:

👉 early financial record control matters enormously.

The SF-86 Stage

Many Guideline F issues first appear during completion of the:

👉 SF-86 Security Clearance Form

This is where applicants disclose:

- delinquent debt

- tax problems

- collections

- bankruptcy

- judgments

- repossessions

- and related financial concerns

The SF-86 becomes:

👉 the foundation of the financial investigative record.

If disclosures are:

- incomplete

- vague

- misleading

- or inconsistent

those problems often follow the applicant throughout the clearance process.

The Credit Report Review

Financial cases often become serious because:

👉 credit reports create documented evidence.

Investigators may review:

- collections

- charge-offs

- judgments

- payment history

- bankruptcy filings

- and delinquent accounts

Applicants are often surprised by how thoroughly these records are analyzed.

The Subject Interview

The:

👉 security clearance subject interview

is one of the most important stages in Guideline F cases.

Applicants frequently damage their cases by:

- minimizing debt

- providing vague repayment plans

- understating financial problems

- emotionally over-explaining

- or failing to provide documentation

This is where many financial cases begin turning into:

👉 credibility problems.

The LOI Stage

If financial concerns remain unresolved, applicants may receive a:

👉 Letter of Interrogatory (LOI)

At this stage, the government is often attempting to:

- clarify debt history

- evaluate repayment efforts

- assess financial judgment

- and determine whether the issue is escalating

Poorly handled LOI responses often become:

👉 the blueprint for later allegations.

The Statement of Reasons (SOR) Stage

If unresolved concerns remain, the applicant may receive a:

👉 Statement of Reasons (SOR)

At this stage:

👉 the issue has hardened into a formal financial-risk concern.

This is where:

- repayment documentation

- tax compliance

- financial recovery

- mitigation evidence

- and strategic framing

become absolutely critical.

The Hearing and Appeal Stage

Some Guideline F cases proceed to:

- DOHA hearings

- written appeals

- or agency review boards

At this stage, adjudicators often focus heavily on:

- whether the debt is currently under control

- whether repayment efforts are genuine

- whether financial behavior has improved

- and whether future financial stability appears likely

This is why:

👉 current financial control matters so much by the hearing stage.

Learn more in:

👉 Security Clearance Hearings and DOHA Appeals

Related Guideline F Resources

For deeper analysis of the most common Guideline F issues, review:

👉 Can You Lose Your Security Clearance for Debt?

👉 Debt and Security Clearances

👉 Can You Lose Your Security Clearance for Bankruptcy?

👉 Bankruptcy and Security Clearances: How Adjudicators Actually Evaluate Financial Risk

👉 Can You Lose Your Security Clearance for Unpaid Taxes?

👉 Can You Lose Your Security Clearance for Collections or Late Payments?

👉 Can You Lose Your Security Clearance for Gambling Debt?

👉 How to Clean Up Your Finances Before Applying for Clearance

👉 What You Should Know About Filing Your Taxes and Security Clearance

How Guideline F Financial Concerns Are Actually Mitigated

Many applicants assume that once serious debt appears in the clearance process, the case is effectively over.

That is not true.

In reality, many Guideline F cases are highly mitigable when the issue is handled strategically and the record is built correctly.

The key is understanding what adjudicators are actually evaluating:

👉 financial responsibility

👉 repayment effort

👉 tax compliance

👉 financial judgment

👉 documentation

👉 future stability

👉 and whether the applicant still appears vulnerable to financial pressure

Strong mitigation often involves:

- establishing payment plans

- filing missing tax returns

- documenting hardship

- stabilizing finances

- reducing delinquency patterns

- proving active financial control

- and demonstrating that the issue is unlikely to recur

For a deeper breakdown of what actually helps—and hurts—Guideline F cases, including debt, bankruptcy, taxes, collections, gambling debt, and financial recovery strategy, review:

👉 How to Mitigate a Guideline F Financial Considerations Security Clearance Concern

What Actually Wins Guideline F Cases

Most applicants think Guideline F cases are won by proving:

👉 “I don’t have debt anymore.”

That is not how adjudicators typically approach these cases.

What actually wins Guideline F cases is:

👉 proving financial responsibility despite financial hardship.

That means the strongest cases usually involve applicants who:

- explain the cause of the financial problem credibly

- document hardship appropriately

- establish repayment or resolution efforts

- file taxes and maintain compliance

- show current financial stability

- avoid new delinquency patterns

- and demonstrate responsible financial behavior going forward

This is one of the most important realities of Guideline F:

👉 the issue is rarely financial perfection.

The issue is:

👉 whether the adjudicator believes the applicant is financially reliable going forward.

Decision Language Explained (What These Terms Actually Mean)

Guideline F cases contain language that often sounds vague or intimidating.

Understanding these phrases gives you a major strategic advantage.

“Financial Considerations”

This refers broadly to financial behavior that raises concern about:

- judgment

- reliability

- responsibility

- vulnerability

- or willingness to meet obligations

“Inability or Unwillingness to Satisfy Debts”

This is one of the most common Guideline F phrases.

The issue is often not simply debt itself.

It is whether the applicant appears:

👉 unwilling or unable to deal with obligations responsibly.

“Good-Faith Effort”

This refers to active efforts to resolve financial problems.

Examples may include:

- payment plans

- settlements

- counseling

- bankruptcy

- tax agreements

- or documented repayment activity

“Circumstances Beyond the Person’s Control”

This is one of the strongest mitigation themes in Guideline F.

Examples may include:

- illness

- divorce

- layoffs

- military relocation

- business failure

- or economic hardship

But adjudicators still evaluate:

👉 how the applicant responded afterward.

“Unexplained Affluence”

This refers to wealth or assets that appear inconsistent with known legal income.

The concern is:

👉 whether the money came from improper or undisclosed sources.

“Unresolved Concern”

This phrase drives many denials.

It means:

👉 the adjudicator still believes the financial situation creates security concern.

“Clearly Consistent With National Security”

This is the actual approval standard.

It means:

👉 the adjudicator feels comfortable defending approval despite the financial record.

If that comfort does not exist:

👉 approval usually does not happen.

Frequently Asked Questions About Guideline F

Can debt cost me my security clearance?

Yes.

Debt can affect your clearance when it suggests unresolved financial instability, irresponsibility, or vulnerability to pressure.

But debt alone does not automatically result in denial.

How much debt is too much?

There is no automatic dollar threshold.

Adjudicators evaluate:

- the cause of the debt

- repayment efforts

- current stability

- and whether the debt appears responsibly managed

Is bankruptcy a clearance killer?

No.

Bankruptcy can sometimes help mitigation when it demonstrates responsible effort to resolve overwhelming debt.

Can unpaid taxes cause denial?

Yes.

Especially where:

- returns remain unfiled

- payment plans do not exist

- or the issue was ignored for years

Tax cases are often treated very seriously.

Do collections matter?

Yes.

Especially when collections are:

- unresolved

- ignored

- repetitive

- or undocumented

What if my debt came from divorce or medical problems?

That often helps mitigation.

But adjudicators still evaluate:

👉 what you did afterward to regain financial control.

What if I am on a payment plan?

Payment plans can be very strong mitigation evidence when:

- they are documented

- current

- and realistic

Should I file bankruptcy before applying for clearance?

Sometimes bankruptcy can improve a case by stabilizing finances.

But timing and circumstances matter enormously.

What if I forgot to disclose debt?

That may create a:

👉 Guideline E — Personal Conduct

problem in addition to Guideline F.

Honest correction timing matters enormously.

Can I get a clearance with bad credit?

Often yes.

Many applicants with poor credit still obtain or maintain clearances when the financial issues are properly mitigated and responsibly managed.

Why National Security Law Firm

Most law firms approach Guideline F cases by focusing only on debt amounts.

That is not enough.

At National Security Law Firm, our security clearance lawyers understand that Guideline F cases are really about:

👉 judgment, vulnerability, responsibility, and whether the record supports future financial reliability.

Our team includes:

- former adjudicators and federal insiders

- military and national security attorneys

- attorneys experienced in high-risk financial clearance matters involving bankruptcy, tax debt, collections, gambling issues, and financial instability

We do not simply help clients “explain debt.”

We build records designed to make approval:

👉 understandable

👉 defensible

👉 and strategically supportable

Complex cases are reviewed through our internal

👉 Attorney Review Board

This means:

- multiple experienced attorneys review the file

- mitigation strategies are stress-tested before submission

- weaknesses are identified early

- and the case is approached through the same layered institutional lens used by the government

Most clients come to us after receiving advice focused only on paying debt quickly.

But Guideline F cases are not won through repayment alone.

👉 They are won through documentation, financial stabilization, strategic framing, and future trustworthiness.

You can read what clients say about working with our team in our

👉 4.9-star Google reviews

Related Statutes and Guidance

Return to the full statute list in the

👉 Security Clearance Statutes and Regulations

Or explore how these rules are applied in real cases in the

👉 Security Clearance Lawyers Resource Center

If you want to go beyond the rule itself and understand how to actually win under Guideline F—how adjudicators evaluate debt, taxes, bankruptcy, collections, and financial risk—review:

👉 How to Mitigate a Guideline F Financial Considerations Security Clearance Concern

You should also review:

👉 How to Win a Security Clearance Case Using Proven Mitigation and Record-Control Strategies

Speak With a Security Clearance Lawyer Before the Record Hardens

If Guideline F concerns are developing in your case, the most important question is not:

👉 “Do I have debt?”

It is:

👉 “Does the government still believe I am financially reliable, responsible, and unlikely to become vulnerable to pressure—and how do we strategically prove that?”

Because once financial concerns are documented:

👉 they are reused

👉 re-evaluated

👉 and often expanded into broader credibility or reliability concerns across the clearance system

The earlier the issue is strategically addressed, the better the chance of preventing escalation into:

- an LOI

- an SOR

- suspension

- denial

- or revocation

If you want to evaluate your situation before the record hardens against you, you can:

👉 schedule a confidential consultation with a security clearance lawyer

The Record Controls the Case.

SECURITY CLEARANCE DENIED OR REVOKED

If you are appealing a security clearance determination, it is imperative that you obtain experienced legal representation. Doing so will provide you with the best opportunity to obtain or maintain your clearance.

Click Here For a No Obligation, Always Confidential Consultation